Nine’s new world: Less ads, more subs and plenty of AI

Matt Stanton and Martyn Roberts

Nine’s half yearly financial results show a business undergoing a seismic shift, with total TV revenue down, subscription revenue up and fierce ongoing cost cutting. There was also the tantalising hint of AI licensing deals providing future revenue streams.

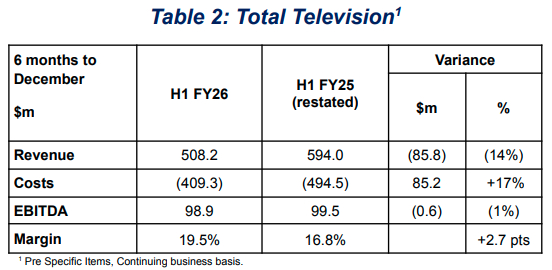

The business posted an EBITDA increase of 6% year-on-year for the second half of 2025. Total TV revenue (free-to-air and on-demand) was down 14%, on the back of the poor ad market and in comparison to a period that included the Olympics the year before. That dragged down group revenue (-5%).

Nine CEO Matt Stanton said the ad market declined 10% in the same period, and described Total TV’s performance as “pleasingly robust”. He rejected a suggestion BVOD platform 9 Now was struggling, saying he was “very pleased with the outlook”.

So……they kept pace with the comparable period last year by taking out costs equal to the amount of revenue that they lost through softer advertising markets.

If anyone remembers, the cost-out was disproportionately focused on the publishing business.

The publishing business looks solid due to “increased ARPU”, translation: consumer price increases.

Both of these things are finite – there are only so many costs you can remove, and only so many times you can increase prices and to a certain level (although it seems like subscription businesses do this every year now), especially if you are removing costs associated with increasing the perceived value associated with that subscription.

In any case, it sounds like they are shaping up for a blood bath, with “the second half of the year….higher proportion of personnel costs” and Gemini being used for “general productivity”.

Not that they can be blamed – if (as is extremely likely) linear TV continues it’s sharp decline especially with larger audiences and ad revenues fall commensurately, it’s going to be a rough decade or so for any legacy media company which isn’t worth being bought out by a streaming giant.